When In Doubt About Market Stability, Invest in Real Estate in a Self-Directed IRA

That’s the advice proffered in an article on TheStreet.com in response to the concerns about Brexit and how it will affect markets. While the world won’t fall apart when the UK exits the European Union, the Brexit vote did bring on market volatility felt around the globe. And, the author tells us, it provided investors with a strong reminder to include real estate and other hard assets in their portfolios.

This is because real estate:

- Tends to hold its value.

- Generates more stable returns.

- Is less vulnerable in volatile economies, unlike paper assets like stocks and bonds.

- Is less dependent on the country’s currency (which can be devalued, which occurred to the British pound following the Brexit vote).

For investors with real estate or precious metals (hard assets) in their self-directed retirement plans the situation is different. Real estate has intrinsic value because it provides shelter, something everyone needs. It can also be leased or traded for other items of value. And it’s not something that is continually created, so that limited supply means there will always be demand. Hard assets are also a hedge against inflation.

For investors with real estate or precious metals (hard assets) in their self-directed retirement plans the situation is different. Real estate has intrinsic value because it provides shelter, something everyone needs. It can also be leased or traded for other items of value. And it’s not something that is continually created, so that limited supply means there will always be demand. Hard assets are also a hedge against inflation.

Investors who have self-directed retirement plans are including real estate, precious metals, many types of commodities and other alternative assets in these plans rather than the soft assets that are highly subject to market volatility. When it comes to real estate, these investments could be rental property, vacation property (domestic or foreign), warehouses, raw land or farm land—real estate that will produce income for the retirement plan and grow the portfolio’s value with the same tax advantages of typical retirement plans. As with all types of self-directed investments, all income and expenses related to the asset flow through the IRA. If the account holder has a Roth or Traditional IRA, the same IRS guidelines apply as they do for plans that are not self-directed.

Real estate professionals are also seeing the value of investing in what they know and understand, and are including real estate in their self-directed retirement portfolios. Since self-directed investors make all their own investment decisions and conduct their own (thorough!) research about their desired investments, including real estate in a self-directed IRA can make good sense for those who already work in that field—or for people who are already investing in real estate outside of their existing IRA.

Want to know more about including real estate in a self-directed retirement plan? Read more on our website and watch our informative video about completing a Next Generation Trust Services real estate purchase kit. Or contact our helpful team at Info@NextGenerationTrust.com or 888.857.8058 for answers to your questions or help getting started on your real estate IRA.

Americans are Underutilizing IRAs

Raise your hands if you took a course in high school or college about IRAs and saving for retirement.

We thought so.

There is a keen need in the United States for more education on the importance of saving for retirement and on retirement plans, especially among young workers; 35 percent of millennials say they don’t know enough about these accounts to consider using one, according to a TIAA survey released Wednesday.

We’ve written many times about Americans’ lack of retirement savings and lack of good savings habits. This was reflected in another result of the survey: 41 percent of people of all ages said they don’t use an IRA but would consider doing so as part of their retirement strategy, down from 56 percent in 2015. A major reason cited was that they believe they don’t have enough money to save any more than they

We’ve written many times about Americans’ lack of retirement savings and lack of good savings habits. This was reflected in another result of the survey: 41 percent of people of all ages said they don’t use an IRA but would consider doing so as part of their retirement strategy, down from 56 percent in 2015. A major reason cited was that they believe they don’t have enough money to save any more than they

already do. What they don’t realize—and why some education is needed—is that they could contribute very small amounts and over time, allow their investment to grow.

That said, it seems that among the respondents of this survey, spending habits are partly to blame. Thirty percent of them said that if they were offered $5000 to spend or invest, they would spend the money on home renovations, a vacation, technology upgrades or a shopping spree. Only six percent said they would contribute the money to an IRA.

Are you utilizing a self-directed retirement plan?

Savvy investors know that investing in alternative assets through a self-directed retirement plan can help them grow a more eclectic and potentially more lucrative retirement portfolio … and that consistently funding their self-directed IRA is a smart habit to attain. Whether funding the plan for future real estate, precious metal or commodity investments, or to include loans, private placements or hedge funds, self-directing one’s retirement is a great way to take control of your retirement goals.

Need some education about self-direction as a retirement strategy? Our website has load of helpful information to get you started and in the know, and the helpful professionals at Next Generation Trust Services will answer your questions and handle your transactions with expertise and efficiency. Contact our office at Info@NextGenerationTrust.com or 888.857.8058.

Need some education about self-direction as a retirement strategy? Our website has load of helpful information to get you started and in the know, and the helpful professionals at Next Generation Trust Services will answer your questions and handle your transactions with expertise and efficiency. Contact our office at Info@NextGenerationTrust.com or 888.857.8058.

Want to know more? Check out this link or watch our informative videos. You can also download our free white paper that gives you the inside scoop on how to use self-direction to build your retirement nest egg, using nontraditional investments you already know and understand.

5 Easy Tips for Self-Directed Beginners

You may have read our previous article about Self-Directed IRAs, and now you’re interested in starting one of your own. Self-directing can be easy, but in the beginning it can seem like there’s a lot of information being thrown at you at once. I have compiled a list of 5 tips that can help you navigate through the process of starting your retirement nest egg.

- Choose the Type of IRA

This is one of those things that’s easier said than done. There are actually quite a few different types of IRAs for you to choose from, and that can make the decision a bit overwhelming. Many people stick with a Traditional or a Roth IRA. Both have their advantages and are simple enough to navigate with once you do a bit of research on each.

- Find the Right Administrator for You

There are many self-directed IRA administrators and custodians out there, and we are one of them. You can call us up and ask us questions about our fees, processing time, anything you’d like really. The only way to know if we’re a good fit for you is to get in touch with us!

- Invest in What You Know

Investing in what you are familiar with can ensure that you are comfortable with your decisions. Do you know a lot about race horses? You can invest in that. Are you a precious metals guru? Go for it! Being comfortable in your knowledge of what you’re investing in makes the process easier. The longer you are investing, the more experience you will gain. As you gain that experience, you can become more comfortable in investing in other things to diversify your portfolio.

- Research Your Investment Further

You’ve probably heard this before, but be sure to research investments. As previously stated, investing in what you know can make you more comfortable with investing. With the added knowledge from your research on your investments, you can get an idea of what to expect on your returns.

- Open and Fund Your Account

Congratulations! You have chosen the type of IRA you want, you’ve decided on an administrator that has your best interest at heart, and you’ve even picked your investment. Once you open your account, you’ll need to fund it in order to start your investments. There are a few ways that you can fund your accounts; such as transfers, rollovers, and contributions. If you’re just starting out on your first IRA, it’s likely that you will be funding your account with contributions. You can find a helpful list of contribution limits here.

Next Generation Trust Services is here to help you build your retirement nest egg. For more information please email Info@NextGenerationTrust.com or give us a call at 888.857.8058.

Retirement on a Budget

Many millennials feel the pressure of student loans bearing down upon them and it can be terrifying trying to figure out how to get rid of all of that debt. On top of worrying about your current financials, you have everyone under the sun telling you to plan for your retirement. You’re probably thinking, “With WHAT money!? How can I get out of debt while saving for retirement at the same time?”. It can seem overwhelming. That’s where Self-Directed IRAs can come in handy for you.

The Basics: Traditional and Roth IRAs

An IRA is an Individual Retirement Account. These accounts are provided by an assortment of financial institutions and they are tax advantaged. There are a few different types, but for now we’ll stick with the basic two: Traditional IRAs and Roth IRAs. Traditional IRAs are tax deferred accounts. What this means is that in addition to the tax deduction you receive for contributing to your IRA, your earnings within the IRA (interest and gains) are also deferred until you distribute. When you withdraw money from your IRA, it is taxed as ordinary income. Roth IRAs are a bit different. There are contribution limits for Roth IRAs and the contributions you make are not deductible. The big draw for a Roth IRA is if you meet certain requirements when you take money out, it is tax free.

The Beauty of Self-Directing

With an IRA you can invest in things like stocks and bonds. With a self-directed IRA, your options become a little broader. Are you well versed in real estate? You can invest in that. Do you like the security of precious metal investments? Invest away! Maybe you’d like to invest in a business? No problem! With self-direction you can pick something that you are familiar with and invest to your hearts content. When you self-direct, you are in the driver’s seat. You can invest in ways that other IRAs and 401ks can’t.

Having a wider array of investment options isn’t the only bonus of self-directing your IRA. It may seem like you need a lot of money to start investing. The truth is you can start with whatever you feel comfortable with. Once you begin investing, you’ll gain the experience you’ll need to feel more comfortable with your decisions and invest more. Investing your money can seem scary at first. You can go your own pace and stick with what you feel most comfortable with.

If you would like to learn more about self-direction, contact us here at Next Generation Trust Services. We would be more than happy to answer any questions you might have. You can reach us at Info@NextGenerationTrust.com or 888.857.8058.

Saving for Retirement? Discipline Yourself with a Self-Directed Retirement Diet

Planning for retirement is often like dieting—the end goal may seem a long way off. So, how can you ensure that you are not that person who complains that they need to lose weight and then never does (or, in this case, find yourself coming up short in retirement)?

Like dieting, retirement is a marathon, not a sprint. The golden rule: Keep your goal top of mind daily and every bit helps. Here are some tips to bring discipline to your retirement planning:

- Think before you spend. Yes, life is full of necessities—food, shelter and clothing. However, do you really need to eat out (or take in) five nights a week? Perhaps you can cut back to once or twice a week and put the savings into a self-directed IRA. (See Number 3.)

- Contribute often and regularly. This is where the self-control comes in. It’s kind of like laying off the carbs in your diet—just do it! Reduce your spending, increase your savings and contribute to a self-directed IRA. (See Number 3.)

- Save with a self-directed IRA. Everyone should have a special savings vehicle earmarked for retirement. This approach will ensure that all your hard work pays off in retirement. By investing these funds wisely in the alternative assets allowed in these retirement plans, your account will grow.

When you discipline yourself with a retirement diet that’s as simple as 1, 2, 3, the numbers add up and with compounding, the results can be pleasantly surprising.

Now, about those alternative assets

Savvy investors who put their retirement funds in a self-directed retirement plan can build their retirement wealth more aggressively. This investment vehicle allows individuals to invest in what they know and understand, and might already be investing in outside of their existing plan. They can follow their hearts (and minds) by including assets like precious metals, real estate, private placements, commodities, hedge funds, or loans … the types of nontraditional investments that are not allowed within typical retirement plans.

Savvy investors who put their retirement funds in a self-directed retirement plan can build their retirement wealth more aggressively. This investment vehicle allows individuals to invest in what they know and understand, and might already be investing in outside of their existing plan. They can follow their hearts (and minds) by including assets like precious metals, real estate, private placements, commodities, hedge funds, or loans … the types of nontraditional investments that are not allowed within typical retirement plans.

At Next Generation Trust Services, our professionals are available to answer questions about self-directed retirement plans and the types of nontraditional investments allowed in these plans. Our transaction specialists make certain that you are investing within IRS guidelines. However, since we do not give investment advice, we strongly recommend you consult your trusted financial advisors about your investments and any tax implications they have for your unique situation.

Feeling disciplined about your retirement savings?

Download our white paper that has lots of helpful information; you can also contact Next Generation at 888.857.8058 or Info@NextGenerationTrust.com, or read through our Starter Kits to open your self-directed retirement account.

A Retirement State of Mind

With many companies foregoing offering their employees retirement plans, many states are taking it upon themselves to fill in the foreseeable financial gap. In fact, four states—California, Illinois, Oregon and Washington—have passed laws paving the way to offer state-run retirement plans, and 18 additional states are considering such a measure.

According to Richard Hiller, senior vice president and head of national government and religious markets at TIAA-CREF in Denver, states are jumping on the bandwagon to offer retirement plans because the “the number of people in the workforce not covered by any retirement plan is pretty staggering—around 50 percent.”

Mix and match

On paper the Department of Labor (DOL) proposed rules for state-run plans sound good; however, industry trade groups like the Investment Company Institute (ICI) raise a number of issues with this approach. They argue that such plans will create an unlevel playing field between states and the private sector as well as the potential to create different rules for different states.

On paper the Department of Labor (DOL) proposed rules for state-run plans sound good; however, industry trade groups like the Investment Company Institute (ICI) raise a number of issues with this approach. They argue that such plans will create an unlevel playing field between states and the private sector as well as the potential to create different rules for different states.

What’s an individual planning for retirement to do? Carpe diem … and take control with a self-directed retirement plan.

Peaceful state

To prepare for a happy and secure retirement, everyone should get with the program and start building up their nest eggs by funding a retirement plan (Traditional or Roth IRA) as often and as much as possible. Financially savvy investors can boost themselves into a better state of retirement income by self-directing their retirement plan.

To prepare for a happy and secure retirement, everyone should get with the program and start building up their nest eggs by funding a retirement plan (Traditional or Roth IRA) as often and as much as possible. Financially savvy investors can boost themselves into a better state of retirement income by self-directing their retirement plan.

For those who understand nontraditional investment options, a self-directed IRA can be a great way to build retirement wealth more aggressively. This investment vehicle allows individuals to include alternative assets they already know and understand, but which are prohibited in typical retirement plans. These include real estate, mortgages, loans, private hedge funds, precious metals, limited partnerships, commercial paper, and more.

Self-directed IRAs can provide informed investors the ability to develop a more diversified portfolio that they control. A self-directed retirement plan allows the individual to respond to economic downturns or take advantage of opportunistic (and tax-advantaged) investments with greater flexibility. The administrator of these plans—like Next Generation Trust Services— handles all the details of the transactions, holds the assets, and manages all account administration and paperwork.

At Next Generation, our professionals are available to answer questions about self-directed retirement plans and our transaction specialists ensure you are investing within IRS guidelines. Since we do not give investment advice, we strongly recommend you consult your trusted financial advisors about your investments and any tax implications they have for your unique situation.

Want to put your retirement plan in a better state? Contact Next Generation at 888.857.8058 or Info@NextGenerationTrust.com, or read through our Starter Kits for more information.

Special Processing Fees for Self-Directed Retirement Accounts: When and Why They Occur

As part of our transaction process, we conduct an administrative review. This review may also alert us to potential prohibited transactions that could have an adverse effect on the tax-advantaged status of your account. Our office prides ourselves on superior customer service so we are more than glad to assist clients in answering questions on our forms, and educate associated people involved in the transaction on compliance review. However, there are certain situations in our account and asset review process that may trigger special processing fees.

These fees arise when the review being performed is outside the normal scope of account administration and transaction review, and special services must be rendered in order to properly execute the transaction.

Our Fee Schedule defines special services as research or special handling of a transaction. In these instances, we must conduct specific research to determine if the asset is feasible for us to hold or not. Special processing may also occur if we must do an unusual review, or one outside our usual scope, to an existing asset within an account. This occurs for a variety of reasons which include but are not limited to these most common examples:

The established details of an asset purchase agreement have not been met or followed, so further review is required.

The established details of an asset purchase agreement have not been met or followed, so further review is required.- Information has been received confirming that a prohibited transaction has taken place and we must begin to distribute the account within 14 days (according to IRC 4975).

- The client has been unresponsive to requests for information, documentation, and/or past due balances.

- Receipt of a request for substantial account research, which can include copies of a closed account file, information about a sold asset, check copies, etc.

- Requested statement from a staff member on letterhead.

In the event a transaction triggers a special processing fee, clients are notified prior to the fee being assessed as a courtesy. The minimum fee is $150 which covers up to an hour of time for our staff to fulfill the research and review requirements; additional time is billed at $150/hour.

That said, we are happy to report that the majority of our clients have not been assessed this special processing fee. Thanks to the wealth of information about self-directed IRAs available on our website and elsewhere, many of our clients are well-educated about the types of assets they can (or cannot) include in their plans and they are proactive about the alternative assets held by their IRA.

As always, everyone at Next Generation Trust Services is happy to assist clients by answering questions about our forms and discuss compliance issues regarding the nontraditional investments allowed in self-directed retirement plans. Don’t hesitate to contact us at Info@NextGenerationTrust.com or 888.857.8058.

Including Gold in Your Self-Directed IRA? Beware of Counterfeit Coins!

Many self-directed investors include precious metals in their self-directed retirement plans. To qualify for a precious metals IRA investment, these assets must meet minimum fineness requirements as set by the IRS (with one exception, the Gold American Eagle). They are as follows:

- Gold: .995 fine

- Silver: .999 fine

- Platinum: .9995 fine

- Palladium: .9995 fine

However, it appears that recently, all that glitters may not truly be gold, according to an article on Investment U from The Oxford Club. The author warns against buying gold coins from eBay, Craigslist, or any vendor that does not guarantee the coins’ authenticity. This is because counterfeit coins from China have been flooding the market. Therefore, (as always) investors are well advised to do their due diligence about the source of these assets. According to a source quoted in the article, these counterfeit coins are being sold to “unscrupulous distributors” through sites such as Alibaba.

Fake gold bar filled with tungsten.

These coins from China are made to look like gold bullion coins but are made out of different metals including lead, zinc, and tungsten. Some metals, like tungsten, have a similar density to gold, which makes a very convincing fake. No matter how real they look, these are definitely not what anyone may include in a self-directed retirement plan! The author states that, “Factories in China are busy churning out thousands of fake American Silver Eagles, Canadian Maple Leafs and U.S. Buffalo coins. They’re sold everywhere from flea markets to eBay and Craigslist.”

Avoid those counterfeits and protect your investment strategy by making sure your precious metal investment comes from a reputable source.

- Your bullion dealer should be well seasoned, someone you know and can verify.

- The dealer must have counterfeit-proofing measurements in place to assure no fake product is brought into their inventory; a new device called a Precious Metals Verifier specifically checks for counterfeits and can test most coins that in album sleeves or plastic cases.

- And the bullion dealer must guarantee the authenticity of every product.

If not, find another dealer who can meet these operational standards. Another word of advice in the article is to buy from established dealers who have relationships with government mints. Ask if the dealer’s staff is periodically trained in counterfeit detection as well.

Don’t endanger your self-directed IRA with fakes—any gold coin investment should come with a full guarantee of authenticity from a reputable dealer. Have a question about including precious metals in your retirement plan? Want to understand better how that works? Contact Next Generation Trust Services with your questions about these and other alternative assets at Info@NextGenerationTrust.com or 888.857.8058. You can also read more about investing in precious metals in this article on our website.

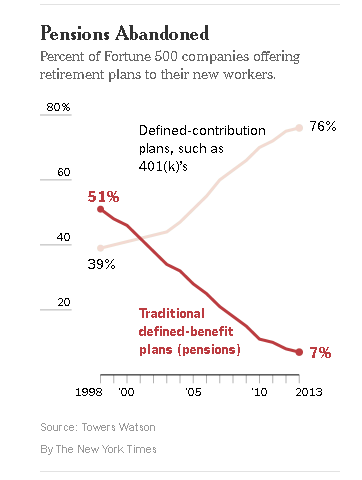

The Death of the Pension Fund

The Urgent Need for a New Retirement Strategy (Hint: It’s Self-Directed)

Many economists acknowledge and write about the problem of Americans’ lack of preparation for retirement. We don’t save enough—many have virtually nothing set aside for their post-employment years.

Many economists acknowledge and write about the problem of Americans’ lack of preparation for retirement. We don’t save enough—many have virtually nothing set aside for their post-employment years.

One issue that has contributed to this, according to Wall Street executive Steve Rattner, is that pension plans—the defined benefit plans that were so popular at one time as a perquisite—are disappearing. Just as the Social Security Trust Fund is becoming unsustainable, and not a given for retirees in the foreseeable future, pension funds have also become unsustainable for employers faced with mounting costs and increased regulatory burdens. Taking their place were defined contribution plans such as 401(k)s.

The problem is, Rattner reports that only about 10 percent of participants in these plans actually contribute the maximum amount allowable … so those folks are falling behind on their retirement savings. The move to defined contribution plans has placed a bit of a burden on participants, who must become more knowledgeable about their investment options (typically stocks, bonds, and mutual funds). Depending on the plan offered by the employer, account holders are expected to allocate their assets, evaluate mutual funds, and select individual stocks.

The problem is, Rattner reports that only about 10 percent of participants in these plans actually contribute the maximum amount allowable … so those folks are falling behind on their retirement savings. The move to defined contribution plans has placed a bit of a burden on participants, who must become more knowledgeable about their investment options (typically stocks, bonds, and mutual funds). Depending on the plan offered by the employer, account holders are expected to allocate their assets, evaluate mutual funds, and select individual stocks.

Of course, we all know how things go when people rely strictly on the stock market—just look at the history of stock averages over the past 15 years! (Buckle up kids, it’s a bumpy ride.) Rattner cites these statistics: “In the first quarter of 2016, domestic mutual funds—a favorite investment vehicle for these retirement accounts despite their chronic underperformance—had their poorest showing in nearly two decades. Through June 15, the 20 most popular funds for 401(k) assets were up 0.6 percent so far in 2016, compared with 2.4 percent for the Standard & Poor’s index.”

The author goes on to talk about revamping the 401(k)s but at Next Generation Trust Services, we have a better idea: open a self-directed retirement plan and take control of your future.

Now, we know that self-direction is not for everyone—but it is a great strategy for savvy investors who really understand the many investment options available on the market, from the traditional to the broad array of alternative assets these plans allow. Sick of the stock market roller coaster? Consider including commodities in your self-directed retirement plan. Don’t like how T-bills are performing these days? What about including real estate in your self-directed IRA? The possibilities are numerous.

Now, we know that self-direction is not for everyone—but it is a great strategy for savvy investors who really understand the many investment options available on the market, from the traditional to the broad array of alternative assets these plans allow. Sick of the stock market roller coaster? Consider including commodities in your self-directed retirement plan. Don’t like how T-bills are performing these days? What about including real estate in your self-directed IRA? The possibilities are numerous.

If you are already investing in alternative assets outside of your existing retirement plan, you could be building tax-advantaged retirement wealth through self-direction, with nontraditional investments that aren’t allowed in typical plans. If you are someone comfortable doing the research required to make these investments wisely, and are comfortable making your own investment decisions, we say “go for it!”

So, rather than relying on those stock-based or mutual-fund-dependent 401(k) plans from an employer, find out more about self-directed retirement plans—perhaps you can even self-direct your employer-based plan. It’s worth asking.

At Next Generation Trust Services, we’re committed to helping more people self-direct their retirement plans by providing information and education about how self-direction works, as well as what you may include (and what you may not). Our team of professionals is available to answer your questions or help you get started; you can contact us at Info@NextGenerationTrust.com or 888.857.8058. If you’re a true self-starter, go to our Starter Kits to get your self-directed retirement account open.