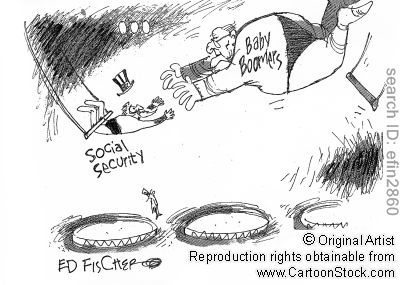

Social Security Raises? Not so Much

As reported in a story on cbsnews.com, many people are bound to be disappointed by the cost of living adjustment (COLA) on next year’s Social Security benefits. It is said that Social Security recipients and federal retirees numbering in the millions will only get a 0.3

percent increase in monthly benefits in 2017. That marks the fifth year in a row of what was termed “historically low raises.” Since 2008, the COLA has been above 2 percent only once (2011). It’s been zero three times, including last year.

The COLA is based on a government measure of consumer prices (the Consumer Price Index for Urban Wage Earners and Clerical Workers, a broad measure of consumer prices generated by the Bureau of Labor Statistics); if prices go up, benefits go up and if prices drop or stay flat (as we’ve seen with gas prices, for example), benefits stay the same.

This adjustment affects more than 70 million people (about 20 percent of the American population). That figure includes not only retirees but the disabled, spouses and children. The COLA also affects people who receive Supplemental Security Income (SSI), the disability program for the poor. According to the article, the average monthly Social Security payment is $1,238, so that miniscule increase? That comes out to less than $4 a month for those average check amounts.

This adjustment affects more than 70 million people (about 20 percent of the American population). That figure includes not only retirees but the disabled, spouses and children. The COLA also affects people who receive Supplemental Security Income (SSI), the disability program for the poor. According to the article, the average monthly Social Security payment is $1,238, so that miniscule increase? That comes out to less than $4 a month for those average check amounts.

Adding salt to that wound for older adults is that Medicare Part B premiums are expected to increase next year—probably higher than that COLA. These premiums are typically deducted from Social Security payments.

Two federal laws come into play here:

1 – The dollar increase in that Medicare Part B premium cannot exceed a beneficiary’s cost-of-living raise—which thereby protects the majority of Medicare recipients. However, that means the burden of that increase will fall on new enrollees and higher-income individuals.

2 – That’s because, according to another federal law, the Part B premium must raise enough money to cover 25 percent of expected spending on doctors’ services.

Yikes!

We’ve said it before – you cannot rely solely on Social Security

Of course, as a company in the retirement industry, we are always going to promote saving for retirement and we hope you are doing so! Whether through an employer-sponsored retirement plan or your IRA, putting just a little aside every month adds up over time, which is why it’s also smart to start saving as early as possible. Given the dire situation with Social Security benefits, it’s not looking hopeful for today’s younger workers to receive substantial payments upon their retirement.

Of course, as a company in the retirement industry, we are always going to promote saving for retirement and we hope you are doing so! Whether through an employer-sponsored retirement plan or your IRA, putting just a little aside every month adds up over time, which is why it’s also smart to start saving as early as possible. Given the dire situation with Social Security benefits, it’s not looking hopeful for today’s younger workers to receive substantial payments upon their retirement.

Plus, with these miniscule-to-no cost-of-living adjustments, those Social Security checks don’t go very far today … and will cover even less in the future when it comes to living expenses (and medical expenses) in retirement, especially with Americans living so much longer than prior generations.

The antidote to the Social Security blues? Be sure to save, of course … and do so more aggressively by investing in alternative assets through a self-directed retirement plan. If you already are doing so outside of your existing plan, why not open a self-directed IRA (Traditional, Roth or SIMPLE), a self-directed SEP—even a self-directed health savings account—and build up your retirement wealth with what you already know and understand.

Are you investing in real estate? How about commodities like cocoa, sugar, or coffee? What about energy investments? The list goes on when it comes to the types of nontraditional investments you can include in a self-directed retirement plan, with the potential to build a more lucrative (and certainly more diverse) portfolio.

Leave the Social Security benefits for your fun money; get serious about your future through self-directed investing. Our Starter Kits have everything you need to get your new account open and our helpful professionals are available to answer your questions about the many options and benefits of self-direction as a retirement wealth-building strategy. Contact us at 888.857.8058 or Info@NextGenerationTrust.com or check out our free white papers for more information.

Avoid those Speed Bumps on the Stock Exchange; Take the Smoother Road to Self-Directed Investments

In June 2016, the IEX Group was approved to become a stock exchange, prompting the venerable New York Stock Exchange to consider adding a feature that IEX has. It’s called a speed bump, a 350-microsecond delay to trading activities that slows down some orders. IEX has it in place but the NYSE leaders are not fans, saying that this strategy relies on hidden orders that are not visible until filled—dark trading.

What makes stock exchanges such frenzied activity centers is that compete to attract a multitude of publicly visible orders; this attracts more trading and builds confidence in stock prices.

Cognizant of the IEX Group’s ever-so-marginally slower trading, the SEC, after approving IEX to join the stock exchange world, also updated a rule that will compel other markets to honor trades subject to a speed bump.

Investors who self-direct their retirement plans, and include alternative assets in those plans, have lots more to talk about than speed bumps and visible trade orders. They get to talk about including a wide array of nontraditional investments in their retirement portfolios, far beyond traditional stocks, bonds and mutual funds. Self-directed retirement plans can include real estate, precious metals, commodities, private placements and much more, with the account owner in control of his or her investment strategy.

Do you have certain alternative assets that you are familiar with, and would like to include in your retirement portfolio? Consider opening a self-directed IRA with Next Generation Trust Services. Our information white paper explains it all to you, and our Starter Kits can get you on the road to building retirement wealth with what you already know and understand.

Have questions? The professionals at Next Generation can give you the answers and guidance you need on the road to self-directed investing. Contact us at Info@NextGenerationTrust.com or 888.857.8058.

All the Single Ladies … Should Prepare for their Retirement

Hint: a self-directed retirement plan can be a great way to do so.

Regardless of all the societal advances we’ve seen in our country over the past few decades—the rise of the single working woman, same-sex marriages—it still remains an issue: many women will be single in their retirement years. Regardless of marital status in earlier, working years, many women will end up single—as a choice, through divorce or widowhood—later in life. The U.S. Census Bureau reports that 54 percent of women ages 65 and up were single in 2014.

Older baby boomers are still part of the “man as breadwinner who took care of everything” generation, which exacerbates the problem. And let’s face it, it is still overwhelmingly the mother who takes time off from work to raise the children, or becomes the caregiver when family members fall ill or require assistance. Add to those factors the prevailing gender pay gap and that more women work part time than full time, contributing to the fact that over their lifetime, women typically earn less and save less (and, they generally live longer than men, so their retirement horizon is extended). All these elements contribute to many women being behind the financial eight ball historically when it comes to retirement savings.

While younger boomers and Generation X women may have lived or are living a very different kind of lifestyle, and are taking care of their future financial needs more proactively, the fact remains that many women are woefully unprepared financially, and will struggle to maintain their current standard of living after they stop working or enter their senior years.

Retirement preparation – now and later.

There are plenty of measures to take today: Talk to your spouse about beneficiary assignment on all life insurance policies and bank accounts. Meet with a financial planner you trust to discuss your situation now and your potential situation later, especially regarding your Social Security strategy. Take a more active role in managing the household finances. Have long-term care insurance to help with medical costs during your later years. Put yourself on a budget and stick to it.

Propel your retirement preparation through self-direction.

The big step to take: fund your IRA! And, if you are comfortable making your own investment decisions and wish to include alternative assets in your portfolio, open a self-directed retirement plan. After all, today’s workers cannot rely on Social Security for income during retirement, and it was never set up to be the sole source of income for retirees (although this has dramatically shifted over the years). Be proactive and create retirement wealth through investments you know and understand, such as real estate, precious metals, commodities, private placements and many more.

Self-directed retirement plans are administered by third-party professionals, like Next Generation Trust Services, that review and execute the transactions, hold the assets, and manage all the paperwork associated with the plan.

Next Generation Trust Services makes it easy to get started on the path to a more eclectic, and potentially more lucrative, retirement portfolio. In addition to the information available in our white paper on the topic and on our website, our Starter Kits walk you through the steps needed to open and fund a new self-directed retirement plan. Once you’ve carefully researched your investment, send us the instructions to execute your transaction and you’re on your way to being better prepared for your retirement needs.

If you have questions about the various nontraditional investments these plans allow, contact our helpful professionals for answers at Info@NextGenerationTrust.com or 888.857.8058.

Were You Affected by Hurricane Matthew? Beware Investment Scams

Unfortunately, scammers take advantage of Americans’ difficult circumstances when disasters hit, and it seems Hurricane Matthew is no exception.

We’re all familiar (unfortunately) with Ponzi schemes and false trading programs that guarantee high returns. According to the SEC’s Office of Investor Education and Advocacy, there are investment scams related to this recent natural disaster to beware. These scams may be from criminals promoting bogus cleanup and repair companies, and those who target individuals who’ve received lump insurance payments as compensation for damages. The SEC warns that individuals should be extremely wary of potential investment scams related to Hurricane Matthew.

As has happened in the past, such as after Hurricane Katrina in 2005, “Some scams are circulated through spam email, promising high returns for small, thinly-traded companies that supposedly will reap huge profits from recovery and cleanup efforts.” Ugh.

It’s so important to protect yourself against investment fraud and other scams. The first rule of defense, says the SEC, is to be skeptical about any investment opportunity and ask a lot of questions. Of key importance is to ask if the person who contacts you is licensed and if the investment they are promoting is registered with the SEC or with a state. Be sure to check their answers with an unbiased source, such as the SEC or your state securities regulator.

Classic signs of fraud are promises of fast and high profits with little or no risk to you. Forget about it! The SEC publishes a handy resource called Ask Questions: Questions You Should Ask about Your Investments that details other questions you should ask of anyone who contacts you about making any kind of investment. It is also available in Spanish.

If you’re received a lump sum insurance payment, be very careful with how you invest this, as it may have to last you and your family a long time and there could be unforeseen expenses to cover that are related to storm damage. The SEC provides this helpful list of online resources; you can also call the agency’s Office of Investor Education and Advocacy at (800) 732-0330 or place a query using this online form.

- Lump Sum Payouts: Guidance about investing a lump sum payout wisely. Lump Sum Payouts: Questions You Should Ask Yourself before You Invest a Dime.

- Affinity Fraud: This relates to investment scams that target particular groups. Investor Bulletin on Affinity Fraud.

- Ponzi Schemes: Ponzi Schemes: Frequently Asked Questions.

- Saving and Investing Basics: General information about saving and investing. Saving and Investing: a Roadmap to Your Financial Security through Saving and Investing. (Also available in Spanish.)

Self-Directed Investors – Do Your Homework!

The wonderful thing about self-directing your retirement plan—and the alternative assets they allow—is that you, the investor, are in control. As the account owner, you make all your own investment decisions; therefore, it is your responsibility to do thorough research into those investments you intend to include in your self-directed retirement plan.

Whether you wish to include real estate, precious metals, commodities, or unsecured loans in your self-directed IRA—or any of the many other types of nontraditional investments available to self-directed investors—we cannot stress enough the importance of conducting your due diligence before sending us your transaction instructions. As a full-service administrator of self-directed retirement plans, Next Generation Trust Services will review the asset as part of our transaction review, and provide guidance about whether your investment complies with IRS investing guidelines. However, it is up to you, the self-directed investor, to fully understand the investment. We recommend you consult a trusted financial adviser if you have any questions about alternative assets and how they may affect your retirement planning; and of course, you can include the SEC’s handy resources as part of this research.

When you’re ready to make your investment, our professional team will assist you and we can answer your questions about self-direction as a retirement strategy, and about the types of investments that are allowed or that are prohibited. You can reach Next Generation Trust Services at 973-533-1880 or 888-857-8058 or Info@NextGenerationTrust.com.

National Save for Retirement Week is Here!

At Next Generation Trust Services, every day is “Save for Retirement” day, but the third week of October has been declared “National Save for Retirement Week” by Congress. This is a good time to start reflecting on your saving habits. Are you saving enough for retirement? Will you be financially stable when the time comes to stop working?

Many people do not feel as though they are saving enough for retirement. A study conducted by Bankrate.com indicates that 51% of households over the age of 50 regret not saving more for retirement. This survey also shows that 31% of 784 participants said their biggest financial regret was not saving enough for retirement (This survey is still open if you wish to vote!). There are many ways to increase your rate of savings and we have a few that you can get started on today.

- Many people use multiple tax-advantaged accounts to increase the amount they can stash away for retirement. Many employers offer a 401k that you can receive matching contributions up to a certain percentage. Using this to your benefit and adding in your own tax-advantaged accounts can increase your amount saved and lessen the financial burden during retirement.

- Another way to maximize your savings is to invest in entities that you already know and understand. Using a self-directed IRA, you can invest in alternative assets in contrast to ordinary stocks and bonds. By diversifying your portfolio with investments that you are familiar with like real estate, precious metals, or loans, you can maximize comfort with your investments. To find out more about self-directed IRAs, click here.

- Be careful about taking money out of your IRA accounts before you hit age 59 ½. If you take money out of these accounts before this age, you can be hit with a 10% tax penalty on top of normal income taxes that you would have to pay, depending upon the account you own. Any money that is taken out early no longer has a chance to grow in that tax-advantaged

Every day is “Save for Retirement” day at Next Generation, so give us a call to get on the path to control your future – today! You can reach us at 973.533.1880 or call us toll-free at 888.857.8058. If you would like to email us, drop us a line at Info@NextGenerationTrust.com. We look forward to working with you!

Why Millennials are Borrowing from their 401(k) Plans – and Why it’s a Bad Idea

It’s tempting to use those funds in a 401(k) plan to put a down payment on a home or to consider it as your children’s college account. It seems that a number of millennial workers are inclined to do this, according to an article in Investment News.

The author cites a Scarborough Capital Management survey that found that 12 percent of people ages 18 to 34 with 401(k) accounts have pulled money out of them to buy their first home. Of the slightly older millennials and younger Gen Xers (ages 35 to 44), nearly eight percent have done so. Older adults “borrow” from these plans at a lower percentage.

Another reason cited by millennials for using retirement funds: paying for their children’s college. In fact, almost half of the survey respondents said they were considering using 401(k) assets to pay for this expense. The 35-44 year-old-group was at 26 percent.

It seems younger savers might not understand all the ramifications of doing this, such as the fact that the borrowed funds tend not to be replenished or paid back; therefore, account holders lose the potential investment gains their funds could earn over time. Plus, there are limits to how much you can borrow and rules about paying it back, so if taking a loan from a 401(k) is calling your name, you are best served to call your trusted adviser to discuss this first.

Rather than resort to this tactic, which could cost a lot of money over time (in terms of those taxes, penalties, and lost investment returns), why not borrow funds from someone you know who has a self-directed retirement account?

Unsecured loans are one of the many nontraditional investments that self-directed investors can make. These include loans for tuition. The account holder and borrower set up all the terms of the loan, from interest rate to time period; then, the account holder sends the instructions regarding disbursement of funds to the self-directed retirement plan administrator along with the note that was created, who executes the transaction (among other important administrative responsibilities).

As with any self-directed retirement transaction, all income and expenses related to the asset—in this case, the loan—must flow through the IRA. This is not a personal loan between two people; it is a loan between a self-directed IRA and an individual. The retirement account earns interest on the loan, the friend or colleague is able to make the purchase or payment he/she desires, and everyone wins.

In order to protect the self-directed retirement plan’s tax-advantaged status, it’s important that the account holder not make a prohibited transaction to a disqualified person, so always check with your plan administrator before making these arrangements.

If your account is held at Next Generation Trust Services, be sure to contact our helpful professionals for insights into this type of transaction, at Info@NextGenerationTrust.com or 888.857.8058. We will also conduct a comprehensive transaction review to ensure you are conducting a transaction that complies with IRS guidelines.

Direct Response Marketing expert Seth Greene’s Interview with Jaime Raskulinecz

Jamie Raskulinecz, our CEO and founder of Next Generation Trust Services, was interviewed by Direct Response Marketing’s expert and best-selling author Seth Greene on his top-rated podcast! You can listen to Seth and Jaime discuss the self-directed IRA business, marketing strategies, and some of the more creative investment ideas we’ve seen done! You can find more of Seth’s podcasts here.

Getting on Track to Hit a Million

No, we’re not taking about the lottery here. We’re talking about retirement savings. Many millennials believe they won’t hit a million dollars in savings by retirement. In fact, a study done by Wells Fargo showed that 64% of millennials surveyed think they will not hit that million dollar mark. About 41% of millennials have not started to save for retirement yet because they are either paying off their debt, or feel they do not make enough money to get started. A whopping 34% of millennials have an average debt balance of $19,978 and many of them are finding this debt to be holding them back from saving as much as they would like to.

Many millennials have a very realistic approach when it comes to their retirement. About 66% believe that retirees should be responsible for their own financial support, and roughly 75% believe that Social Security will not be around when the time comes for them to retire (You can read more about that here). Millennials understand the importance of taking advantage of their employer-provided 401k plans, but too few millennial employees actually have them – roughly 52%.

It’s easy to see why many millennials might feel discouraged about their future retirement. More than half of millennials (52%) are nervous about investing because of the volatility they have witnessed within the stock market. This Harris Poll from March of 2016 explains how 79% of millennials are not investing in stocks because of this fear of volatility. With half of millennials nervous about stocks, and over three quarters of millennials not investing in stocks at all, how can they get on track to hit a million in retirement savings?

The Mark: How to Hit it

According to Wells Fargo, many millennials could be on their way to hitting the million dollar mark by retirement without even knowing it. The median salary for millennials is $27,900 and about 44% are putting away more than 5% of their income for retirement.

There are many options available to millennials who wish to start their retirement nest egg. A popular option is a Roth IRA. These allow your contributions and investment earnings to grow tax free, as you have already paid taxes on the funds that have entered the account. Another bonus of having a Roth IRA is when you take the money out of that account while in retirement you don’t have to pay taxes on it. If you’re interested in opening a Roth IRA, here is how easy it is.

Once you open a self-directed IRA, you can invest as little or as much as you would like into a multitude of investment types. You can read more about that here and here.

Need some education about self-direction as a retirement strategy? Our website has load of helpful information to get you started and in the know, and the helpful professionals at Next Generation Trust Services will answer your questions and handle your transactions with expertise and efficiency. Contact our office at Info@NextGenerationTrust.com or 888.857.8058.

Want to know more? Check out this link or watch our informative videos. You can also download our free white paper that gives you the inside scoop on how to use self-direction to build your retirement nest egg, using nontraditional investments you already know and understand.

The Low Down on Required Minimum Distributions

You have been an avid saver and have funded your IRA or 401(k) plan diligently over the years. Good for you! However, be aware that once you turn 70 ½ years old, you are required to start taking distributions from your retirement plan. These required minimum distributions (RMDs) are based on a factor from the Uniform Lifetime Table as specified in IRS Publication 590, along with your age and account balance. You are absolutely required to start depleting your retirement plan—including one that is self-directed—upon reaching that magic age.

For account holders of multiple IRAs, a required minimum distribution must be calculated separately for each one. Those amounts can then be totaled and the aggregate amount withdrawn from any one or more of the accounts. In the case of multiple employer plans, the rule is different: calculate and withdraw an RMD from each plan.

The percentage you must withdraw from the retirement plan increases every year. By working with your financial adviser, you can plan ahead for anticipated withdrawal amounts, what to do with the money, and how it will affect your taxes.

Considerations for that first RMD

Account holders must begin distributions no later than April 1 of the year after they reach the age 70 ½. Those who turn 70 ½ in 2016 can wait until April 1, 2017 to take their first distribution. If you fall into that category, we suggest you consult your tax adviser regarding when to take your first distribution. If you wait until the following year, you will also be required to take the distribution for 2017 before year-end, causing you to take two distributions in 2017.

Since taking distributions can raise your taxable income and increase the tax you owe on Social Security, or affect your itemized deductions, it’s best to check with your trusted adviser about the timing for that first RMD.

People who are still working at that age may elect to put off distributions from their employer’s retirement plans if they are not an owner of the business. If this is the case for you, you can wait to start withdrawals until after April 1 following the year that you reach age 70 ½, or when you decide to retire.

Trustee/custodian requirements

Due to IRS compliance mandates, account holders can run but they can’t hide. That’s because any financial firm that serves as the trustee or custodian for your retirement account (including administrators of self-directed retirement plans) must file annual reports with the IRS stating the amount of the RMD for each taxpayer and for each year a distribution is required. Taxpayers who do not follow these distribution requirements can end up paying a very high price: a 50-percent excise tax on the amount of the distribution that is late or insufficient.

RMDs from your self-directed retirement plan

As a third-party administrator of these plans, Next Generation Trust Services follows all IRS requirements concerning the reporting of RMDs for all of our clients. Since self-directed retirement plans allow for so many different types of assets aside from stocks, bonds and mutual funds, there are various tactics to implement in order to take your RMD every year. Our professionals can answer your questions about how to make these transactions within IRS compliance in order to abide by tax laws. Contact us at Info@NextGenerationTrust.com or 888.857.8058 to discuss your particular needs.

As a third-party administrator of these plans, Next Generation Trust Services follows all IRS requirements concerning the reporting of RMDs for all of our clients. Since self-directed retirement plans allow for so many different types of assets aside from stocks, bonds and mutual funds, there are various tactics to implement in order to take your RMD every year. Our professionals can answer your questions about how to make these transactions within IRS compliance in order to abide by tax laws. Contact us at Info@NextGenerationTrust.com or 888.857.8058 to discuss your particular needs.